INVESTMENT STRATEGY

By Sr. Research Analyst, Eagle Mountain Partners – with excerpts from Blackstone | The Connection written by Sean Klimczak, Global Head of Infrastructure. October 31, 2024

With the explosion in data due to the emergence of generational shift towards Artificial Intelligence, there is an urgent need for physical infrastructure to store, process, power and deliver it.

We believe that the intersection of digital infrastructure and the need for power is one of the most exciting and critical investment themes of our time. As Al continues to evolve, the demand for data centers and power will only grow, creating a wealth of opportunities. Eagle Mountain Partners aims to be one of the leaders in this megatrend. We expect the next decade will bring tremendous value to investors who recognize the potential in this space.

The rapid expansion of digital infrastructure and the growing demand for power is a topic on everyone's mind these days. Many are wondering, does the hype really match reality? From our perspective, not only is the hype justified, but the opportunity is far larger than most realize. To fully understand this intersection of digital infrastructure and power, let's start by looking at the drivers behind the Al revolution: data.

The amount of data being generated and consumed is nothing short of extraordinary. Think back to 2006, when cloud computing first emerged. Facebook hit 100 million users by 2008, lnstagram in2013, and Netflix by 2017. In 2022, ChatGPT hit 100 million users just two months after launching, and earlier this year, OpenAI introduced SORA, a text-to-video app that has drawn significant user interest.1The result? Data usage has increased 100 times over the past 15 years, and even more striking, more data has been created in the past three years than in all of history. 2As Al continues to gain momentum, this trend will only accelerate. Global cloud migration is still in its early stages, and with revenues from cloud services expected to more than triple in the next five years, data growth will be astronomical.

But it's not just the sheer amount of data that's growing-it's the intensity of the data being processed. Traditional tools, like Google searches, are lightweight in terms of power consumption. Conversely, a ChatGPT query requires 10 times the power of a Google search and Al-generated images using tools like DALL-E require 50 times the power of a simple Google search. And if you ask SORA to create a video? We're talking 10,000 times the power consumption. 3To put that into perspective, creating a basic Al-generated video is the energy equivalent of charging your phone 119 times. As Al applications become more advanced and widespread, we are just beginning to scratch the surface of what I call the next wave of data intensity.

With this explosion in data, there's an urgent need for physical infrastructure to store, process, and deliver it. This is where data centers come into play. Over the past five years, the number of US-leased data centers has increased 17 times, driven by the rise in cloud computing and Al. This year alone, 5,000 megawatts of data center capacity will be added in the US. 4 That's roughly 1% of the nation's total power consumption about the same amount of power used by Miami-Dade County's 2.7 million people.

The growth of data centers is a global phenomenon. We estimate that the US will see over $1 trillion invested in data centers over the next five years, with an additional $1 trillion invested internationally.5 The scale of these facilities is staggering. The largest data center currently under construction is an estimated 500 megawatts,6 which is equivalent to the power demand of 375,000 homes.7 As a matter of course, OpenAI CEO Sam Altman recently proposed building clusters of 5,000-megawatt data centers across the US,8 each of which would be equivalent to the entire US data center capacity built in the last 12 months.

Regions like Europe and Asia are still a couple of years behind the US in terms of demand growth. But with Asia representing two-thirds of the global population and accounting for just 15% of global data center leasing, the potential for growth in these regions is immense.9

As exciting as the growth in digital infrastructure is, it comes with a significant challenge: the power to support it. Take a look at what's happening in Atlanta, now the second-largest global data center market. Data center demand has increased by 46 times since 2019,10 and as a result, power demand in Georgia is projected to grow by 39% between now and 2030.11 This type of growth is not unique to Georgia-states like Arizona, Indiana, Virginia, and Texas are also contending with 5% or higher annual growth in power demand.12

For a US market that had relatively flat power demand for the past 20 years, this sudden surge is a major shift. As a country, we face the prospect of having to double our power grid's capacity over the next 12 to 13 years to keep up.13 At the same time, the rise of electric vehicles is adding more strain to the grid. Every new EV increases a home's power consumption by 40%. In addition to this strain is the $500 billion being invested in reindustrializing the US with power-hungry factories,14 and it's clear we're dealing with a massive spike in power demand.

On the supply side, things don't look any easier. Roughly 15% of the US power supply is still coal-generated, but those plants are being retired.15 Meanwhile, our grid is aging – on average, it's over 40 years old-and renewable energy sources like wind and solar, while promising, have a capacity factor of only around 30%. 16 This means that backup power from natural gas and battery storage will be crucial to ensuring the grid remains stable.

This convergence of data center growth and rising power demand presents a rare and compelling investment opportunity. Eagle Mountain Partners has strategically positioned itself at the forefront of this trend, to become a strategic global investor in the intersection between data centers, power generation and Al driven infrastructure. We have identified significant upside potential in several areas.

First, data center leasing is set to continue growing as Al and cloud computing expand. Major players like Blackstone have already over $70 billion worth of data center assets, with another $100 billion in the pipeline, including facilities under construction and their announced acquisition of Airtrunk. Many of these assets are backed by long-term contracts with AA-rated counterparties, offering stable, attractive returns. Eagle Mountain Partners has strategically positioned itself as an intermediary between data center developers and large global infrastructure funds.

Second, power generation and utilities, particularly in the renewable space, are poised for significant growth. With trillions of dollars needed to upgrade the power grid, Eagle Mountain Partners believes investments in wind, solar, and natural gas generation will yield strong returns. In particular, we expect significant demand for natural gas pipelines, as renewables require backup power.

Lastly, the broader energy transition, including investments in battery storage, HVAC systems, and transmission infrastructure, presents a meaningful opportunity to capitalize on this megatrend. At Eagle Mountain Partners, we're excited to be leaning into this megatrend and believe we are well placed to deliver value-add to our investors.

Development-focused integrated data center and power projects typically target equity IRRs in the range of 12%–18% on a stabilized basis, depending on leverage, offtake structure, and credit quality of counterparties.

Ground-up hyperscale developments — particularly those incorporating dedicated on-site or adjacent power generation — can achieve 25%–40% equity IRRs over a four-year hold period, reflecting development risk, construction complexity, and the value uplift realized upon stabilization and lease-up. These returns are supported by high operating margins, long-term tenant commitments, and 10+ year power purchase and lease agreements with investment-grade (AA–AAA) counterparties, which underpin financing and materially reduce long-term cash flow volatility.

The hyperscale data center campus, designed for a total IT load of approximately 495 MW, will be developed in multiple phases to align capital deployment with leasing velocity and tenant commitments. The full build-out is expected to occur over a 4–5 year horizon, with each phase encompassing a 24–30 month cycle from design through commissioning.

Each phase follows a replicable, modular development model, comprising multiple data halls across three to five buildings, each supporting 80–150 MW of IT capacity.

The initial anchor phase, typically ranging from 10–60 MW, establishes the core utility infrastructure, on-site substation, and network connectivity. This phase enables early operations and revenue generation ahead of full power plant completion.

Subsequent phases are scaled in line with tenant pre-leasing agreements, expanding the mechanical and electrical backbone within the existing buildings and leveraging shared campus infrastructure. The third phase generally introduces new buildings within the same campus footprint, benefiting from previously provisioned power and fiber capacity, resulting in material construction and timeline efficiencies.

The final phase completes the campus to full hyperscale capacity, driven by tenant expansion requirements and additional anchor commitments from major cloud or enterprise customers. This staged approach optimizes return on invested capital, minimizes demand risk, and enables the project to achieve infrastructure-grade cash flow stability upon full stabilization.

Phase 1 - 10-100 MW - Initial anchor phase, establishes core infrastructure and utility interconnection.

Phase 2 - 100-125 MW - Scales based on tenant pre-leasing; expands mechanical/electrical backbone.

Phase 3 - 125-150 MW - Adds new buildings within the same campus; power and fiber already provisioned.

Phase 4 - 120-150 MW - Final build-out to reach 495 MW; driven by existing tenant expansion or new hyperscale anchor.

The project’s power infrastructure will be developed to ensure long-term scalability and cost efficiency. A 600 MW-capable substation will be constructed during Phase 1, providing sufficient interconnection capacity for the full campus build-out and eliminating the need for future redesigns or system upgrades. Power Purchase Agreements (PPAs) will be structured with incremental capacity step-ups, commencing at approximately 100 MW and expanding in line with tenant demand and data center load growth. To enhance energy resilience and sustainability, each phase may also incorporate 150–200 MW of modular on-site generation, leveraging gas-fired or renewable units as appropriate to support redundancy, optimize energy pricing, and align with customer sustainability objectives.

A data centers financial and operational success is underpinned by long-term contractual relationships with investment-grade tenants and power offtakers. The tier and credit quality of expected anchor tenants is critical to ensure pre-leasing targets and PPA arrangements are achievable. These contractual commitments provide early cash flow visibility, reduce vacancy risk, and establish a strong foundation for subsequent development phases.

Leasing activity and revenue generation will scale in tandem with phased development, with each stage supported by long-term contractual commitments from creditworthy hyperscale tenants. The initial phase is expected to achieve 50–80% pre-leasing prior to commissioning, providing early revenue visibility and underpinning construction financing. As subsequent phases come online, tenant expansions and new pre-leases are anticipated to drive occupancy to 70–90%, benefiting from established infrastructure and proven operational performance. The final phase is projected to reach full stabilization, supported by existing tenant growth and additional anchor commitments from major cloud and enterprise customers. Revenue and EBITDA margins are expected to expand with scale—from approximately 45–50% during initial operations to 60%+ at full build-out—reflecting increasing operating leverage and the efficiency of shared campus infrastructure. This phased leasing strategy enables predictable cash flow growth, mitigates vacancy risk, and enhances long-term portfolio stability.

A phased development approach enables disciplined capital deployment, risk mitigation, and operational scalability, aligning investment timing with tenant demand and market absorption. By sequencing construction in discrete phases, the project avoids overexposure to upfront capital costs while preserving flexibility to adapt to evolving technology requirements and customer specifications. Early phases serve to validate design, infrastructure performance, and leasing velocity, providing a de-risked foundation for subsequent expansion. As the campus matures, later phases benefit from existing power, fiber, and civil infrastructure, resulting in significant cost efficiencies and accelerated delivery timelines. This approach also supports progressive value creation, with opportunities for partial recapitalization or refinancing as stabilization milestones are achieved. Ultimately, the phased model maximizes return on invested capital, enhances financing optionality, and delivers a predictable pathway from early development returns to infrastructure-grade, long-term cash flows.

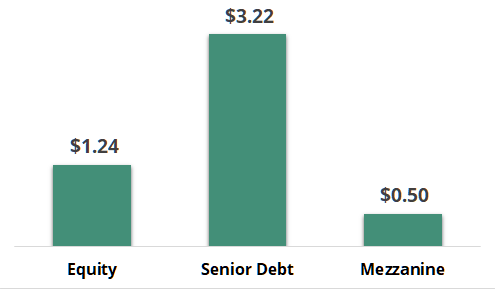

Based on current 2025 market conditions, infrastructure financing standards, and data center development economics, a 495 MW hyperscale data center campus has an assumed mid-range capital cost of $10 million dollars per Megawatt or $4.95 billion total build out. The data center financing structure is a combination of $1.24 billion (25%) in equity with minimum IRR requirement of 16-24% percent and $3.22 billion (65%) of senior debt at a nominal interest rate of 6.5%, on a 12-year amortized loan. This is usually paired with a mezzanine construction loan of $0.5 billion at 10% cost of capital.

The power plant, requiring a reserve and redundancy (plus line losses, maintenance, and N+1 configuration), will need a generation capacity of 550–600 MW at a mid-range capital cost of $1.3 million dollars per Megawatt or $780 million total build out. The power generation financing structure is a combination of $195 million (25%) in equity with minimum IRR requirement of 13-15% percent and $585 million (85%) of senior debt at a nominal interest rate of 6.0%, on a 15-year amortized loan.

Total development capital of approximately $4.95 billion is expected to be deployed across four phases in alignment with construction progress and leasing milestones. Phase 1, representing roughly 20% of total project cost (~$1.0 billion), will be funded through a higher proportion of equity (30–40%) complemented by a construction loan, reflecting the risk/reward profile of the initial development and utility interconnection stage. Phase 2, accounting for approximately 25% of total capital (~$1.2 billion), will be financed through a combination of senior project debt and partial reinvestment of Phase 1 equity returns, benefiting from improved credit strength following initial tenant commitments.

Phase 3 will comprise roughly 27% of total capital (~$1.3 billion) and is anticipated to be financed through a refinancing of earlier phases coupled with new construction debt facilities, as the project transitions toward stabilized operations. The final phase, Phase 4, representing the remaining 28% (~$1.45 billion), will fund campus expansion and build-out to full capacity, primarily through retained earnings and long-term, low-cost debt instruments. This staged financing structure enhances capital efficiency, de-risks the development timeline, and supports attractive equity returns as the project matures toward stabilization.

Phase 1 ($1.0B) - 20% of total - High equity content (30–40%) + construction loan

Phase 2 ($1.2B) - 25% of total - Mix of senior project debt + partial reinvestment of Phase 1 equity

Phase 3 ($1.3B) - 27% of total - Refinincaing and construction draw of insitutional debt

Phase 4 ($1.45B) - 28% of total - Expansion capex financed via retained earnings and long-term debt

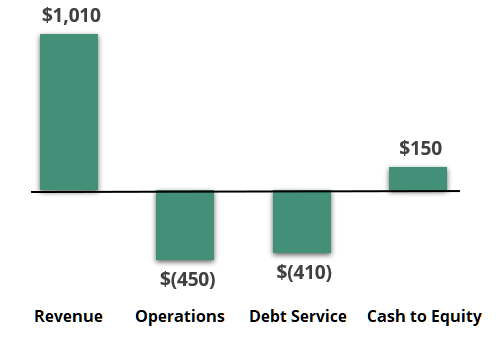

The data center campus, with a power utilization of 90% (445 MW average load), is anticipated to generate $2.28M/MW-year with an EBIDTA margin of 55%. This results in $1.01 billion in annual revenue with an EBITDA of $556 million, less debt service of $410 million. Cash flow to equity will be $146 million per annum with an 11.8% cash yield and a minimum expected equity IRR of 17%+ including terminal value.

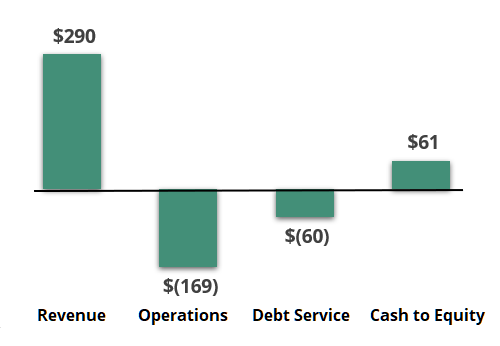

The 600 MW combined-cycle natural gas power plant, operating at an 85% capacity factor, is expected to generate approximately 4.47 TWh per year at a contracted power sale price of $65/MWh. With total annual revenue of $290 million and operating costs of $169 million, the project yields an EBITDA of $121 million. After annual debt service of approximately $60 million, the cash flow to equity is projected at $61 million per annum, representing a 31% cash yield on equity and a minimum expected post-tax equity IRR of 15%+, assuming stable fuel prices and long-term PPA revenues.

All large-scale infrastructure projects carry inherent risks, including construction delays, regulatory approvals, and market demand fluctuations. Acknowledging these risks upfront and demonstrating proactive risk management is key to success. Together with domain experts, data center development mitigates exposure through modular, phased construction, pre-leasing of anchor tenants, long-term PPAs, and conservative financial assumptions. This combination of structural and operational safeguards ensures that while risks exist, they are systematically addressed, reinforcing lender confidence in the project’s resilience and long-term value creation.

Investor returns are supported by tangible, income-producing assets and structured financing. The data center is secured by long-term real estate collateralized with commercial loans, while the power infrastructure uses non-recourse project financing tied to cash flows from long-term PPAs. This dual-layer structure—real estate plus project-level cash flow collateral—mitigates downside risk and provides a stable foundation for equity returns and targeted IRRs.

1. International Data Corporation (IDC), as of May 2024.

2. International Data Corporation (IDC), as of May 2024. Reflects change in data created, stored and consumed in Zettabytes, from 2010 to 2025(2024 and 2025 represent year-end estimates).

3. Represents power consumption requirements. Internet Search & Language AI: Reuters, as of February 22, 2023 (latest available). Image AI: The Register, as of December 4, 2023 (latest available). Video AI: Factorial Funds, as of March 15, 2024.

4. Datacenter Hawk, as of June 30, 2024.

5. Dell’Oro estimates, as of July 31, 2024.

6. NADC, CBRE and Datacenter Hawk, as of June 30, 2023. 2024 reflects BX estimate of Google self -built data center.

7. Gridstor, as of October 28, 2022.

8. Bloomberg, as of September 24, 2024.

9. Datacenter Hawk as of June 30, 2024; Altman Solon as of April 30,2024.

10. Datacenter Hawk, as of June 30, 2024.

11. Reflects Georgia Power expected load growth through 2030 as forecasted in 2021 and forecasted in 2024. QTS Reporting, as of January 2024.

12. (1) Arizona represents long-term electricity sales forecast of Pinnacle West (NYSE:PNW; fully regulated electric utility serving ˜1.4millioncustomers in high-growing cities across Arizona) in 2019 vs. 2024. | (2)Georgia represents utility Georgia Power’s summer peak demand CAGR published in2022 (’22–’41) vs. latest forecast (’23–’30). | (3) ERCOT and PJM are Independent System Operators (ISO) organizations that coordinate, control, and monitor operations of the electrical power system / power capacity market in Texas / the Mid-Atlantic, respectively. PJM is the ISO region that covers DE,IL, IN, KY, MD, MI, NJ, NC, OH, PA, TN, VA, WV, and DC. | (4) Virginia represents Dominion PJM 10-year summer peak demand CAGR published in 2021 vs.2024. | (5) N. Indiana represents NIPSCO peak load forecast published in 2021(roughly flat through ’40) vs. the latest 2nd Draft of the 2024 Stakeholder Integrated Resource Plan (IRP). Uses a forecast period of (’23–’35) and does not include upside emerging load from data centers in revised case. | (6) Texas represents ERCOT summer peak demand CAGR published in 2023 (’23–’32) vs. latest forecast (’23–’30).

13. US Department of Energy, as of August 12, 2024.

14. The White House, as of April 2024. Represents ˜$500 billion committed by corporations into electricity-intensive battery, solar panel, EV,and semiconductor manufacturing facilities.

15. US Energy Information Administration, as of February 2024.

16. US Department of Energy, as of October 2023.